Alphabet Q4 Analysis: Google Cloud Takes The Center Stage

Google's FY 2025 results highlight double-digit growth in Search and Cloud revenues, single-digit growth in YouTube Ad revenue but a modest decline in Ad Network revenues.

So, Alphabet (GOOGL 0.00%↑, GOOG 0.00%↑ ) just released its Q4 and FY 2025 results, and the numbers look pretty impressive.

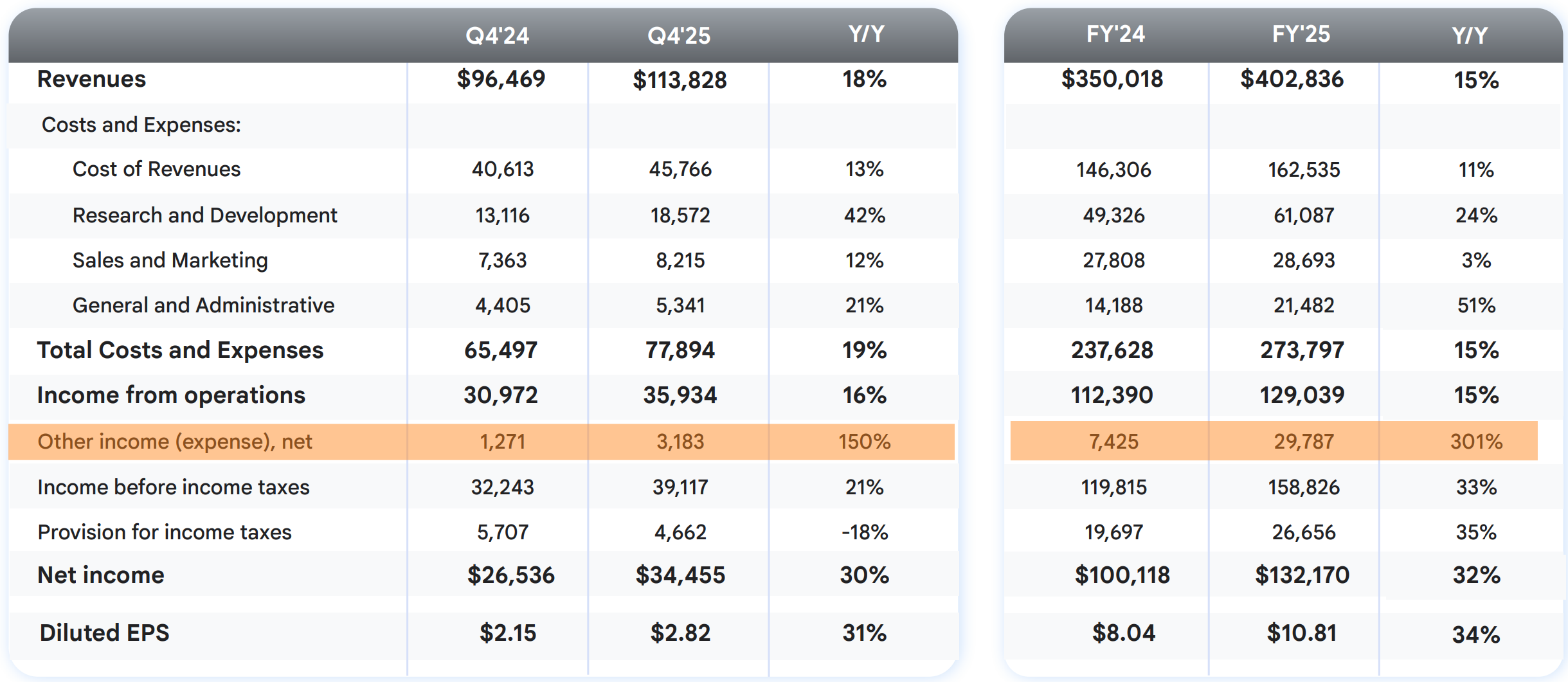

For the Fiscal Year 2025, revenues surpassed $400 billion for the first time, up 15% YoY. Net Income increased by 32%, while EPS increased by 34%. For a company of Alphabet’s size, this kind of double-digit growth is a remarkable feat indeed.

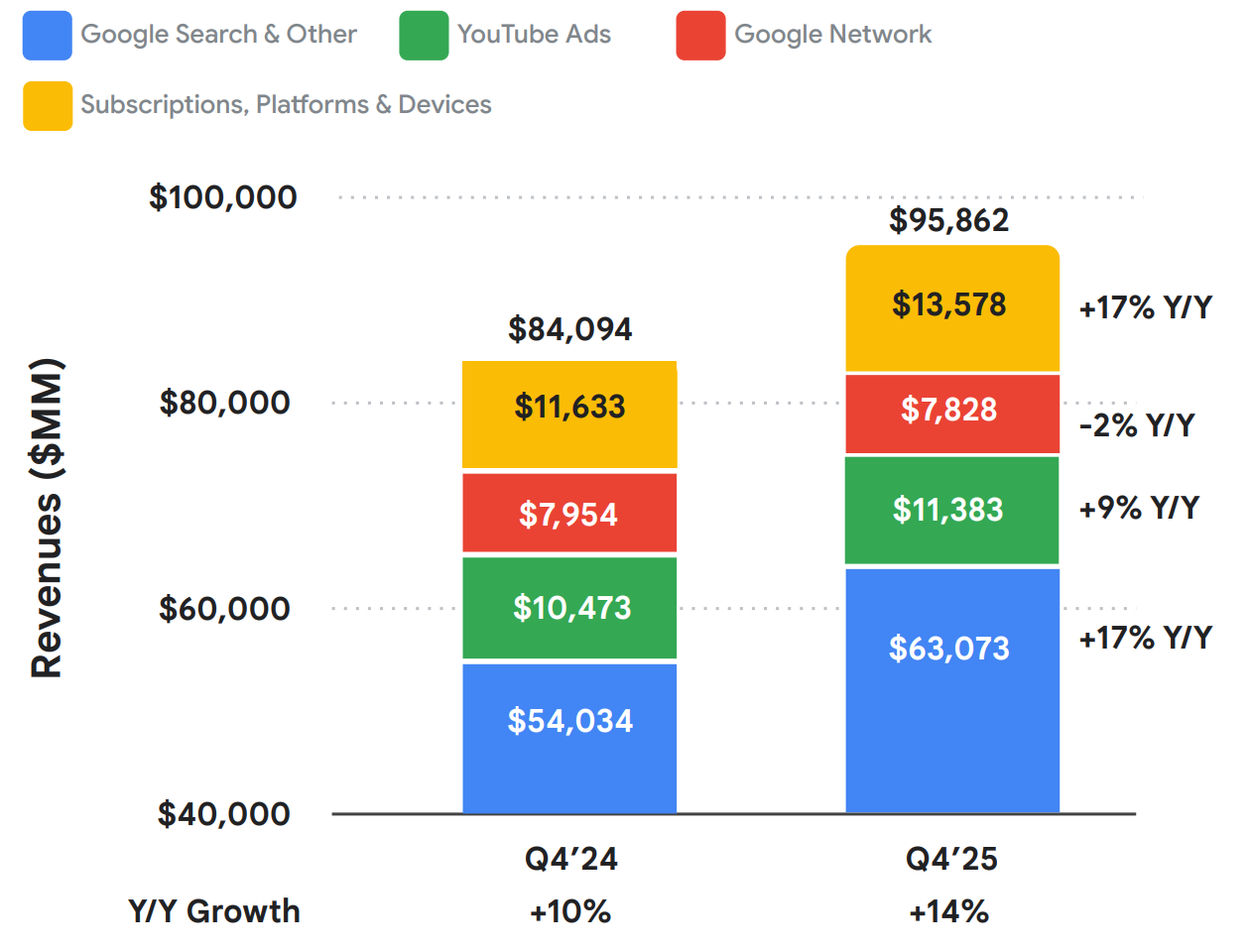

Revenues by Segment

Search & Other, and Subscriptions, Platforms & Devices revenues are up 17% YoY in Q4, YouTube Ad revenues are up 9%, and Google Cloud revenues are up a staggering 48% as well.

But not everything went up this quarter.

Revenues from Google Network Ads actually declined by 2% to $7.8 billion, down from $7.9 billion in Q4 2024. In my opinion, this decline likely comes from declining web traffic due to increased use of AI tools like ChatGPT and Gemini for search queries.

Google Cloud

Nothing (apart from CapEx, of course!) grabbed more eyeballs than the Cloud revenues in yesterday’s announcement. Last year in Q4, Google Cloud brought in approximately $11.9 billion in revenues, whereas this quarter the number jumped to $17.6 billion, a 48% increase. The segment gets even more interesting when you factor in the $240 billion cloud backlog.

Not only that, in addition to accelerating revenues and growing backlog, Google improved operating margins in this segment from just under 18% to close to 30%.

CapEx Keeps Going Up

Everything comes at a cost, and for hyper-scalers like Google, Meta, and others, capital expenditures have been in focus for a while now. In Q4, the company’s CapEx nearly doubled from around $14 billion in Q4 2024 to more than $27 billion, for a full-year total of approximately $91 billion.

For the FY2026, Alphabet expects to spend $175b to $185b, nearly double the FY25 spending. This number surpassed the ~$120 billion mark that analysts expected from the company by a wide margin.

But, in my opinion, for a company that is sitting on a $240b cloud backlog, an increase in overall Ad revenues due to AI developments, the spending seems justified.

Is Google still worth buying?

Google is up ~72% in the last twelve months, and at the time of this writing, the stock is trading at approximately $331. Based on FY2025’s diluted EPS of $10.81, the stock currently trades at a 30.6x multiple, whereas it was trading at a 24x multiple a year ago. The valuation multiple has clearly expanded.

So, a very obvious question is: Is Google still worth buying? The short answer is, yes.

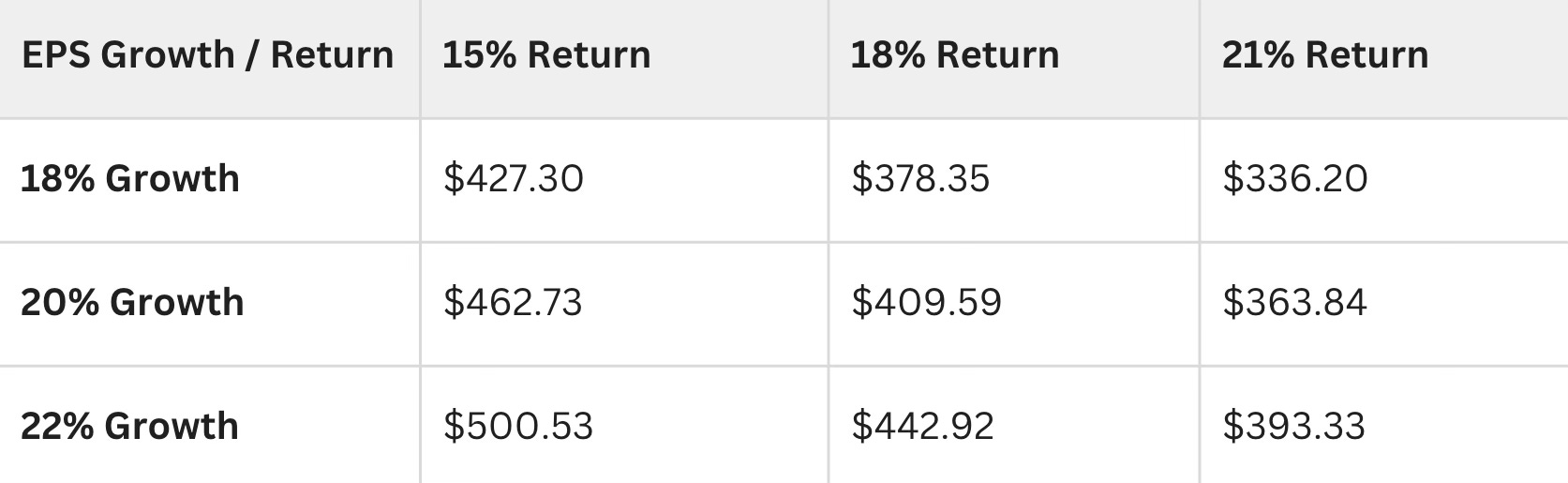

In the base-case scenario, where EPS grows at 18% per year for the next five years, the stock is still trading below its intrinsic value of $336.20, yielding a 21% annual return.

However, if the EPS growth rate falls below 18%, the returns will likely be lower than expected.