Why KKR Is More Resilient Than Most Investors Think

KKR is one of the largest alternative asset managers globally with $723 Billion in AUM. Its stock is currently down ~31% from its peak.

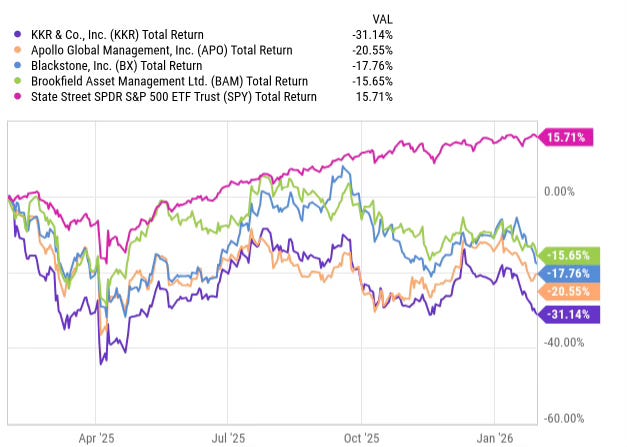

As I write this article, KKR & Co. (NYSE: KKR) has retreated more than 31% from its peak. But it’s not alone. Almost all alternative asset managers are down — some more than others.

So, a very obvious question to ask is: What’s wrong? Is KKR the business struggling just like KKR the stock? Or is there more to the story than the 1-year chart is telling?

I’ll try to answer these questions as I analyze the performance of KKR’s most recent quarter and the growth opportunities that might create long-lasting value for the company. I will also discuss KKR’s valuation at these levels to justify why I think now might be a good time to buy KKR.

Q3 Performance

To begin with, KKR’s Q3 2025 results were really good by all standards.

We saw an increase of 15.3% in revenues and an impressive 43% uptick in net income. And the numbers suggest that expense control played an important role here. Although total expenses did increase by 5.86%, the expenses in the asset management and strategic holdings segment actually decreased by over 21%.

On top of that, KKR’s AUM (Assets Under Management), Fee Paying AUM, and Perpetual Capital all moved upwards. AUM and Fee Paying AUM increased by 16% YoY in Q3, and perpetual capital went up by 19% as well.

This positive change could be attributed to Global Atlantic‘s (KKR’s insurance segment) asset base and strong fundraising. In Q3, KKR raised $43 billion in funding. Dry powder, which is capital that is available to deploy, reached $126 billion.

The reason I’m mentioning these numbers is because they highlight that investors are willing to commit their capital to KKR, and because of its dry powder, KKR wouldn’t be sitting on the sidelines when lucrative opportunities come its way.

Valuation

FRE Margins

An important metric that I pay special attention to whenever I analyze an asset manager is the Fee-Related Earnings ((FRE)) margin.

Since, KKR and other asset managers earn a majority of their revenue by charging fees on capital that is committed to their funds, the FRE margin is essentially an indicator that tells how much of that revenue turns into income.

The FRE margin, in KKR’s case, is the highest in the industry. Not only did it have the highest margin in 2023 (around 62%), I like the fact that the company is still focusing on further improvements. In 2025, the FRE margin touched 69%, which represents a difference of 100 basis points from another industry leader, Blackstone (BX), and much more than other managers.

You might be thinking, but how does KKR pull this off? How does it have these high margins that other asset managers might aspire to?

I’d say the first contributing factor is its emphasis on operational leverage, which simply means increasing revenues without letting fixed costs catch up.

Secondly, KKR has a Capital Markets business which is a very high margin revenue stream. This segment contributes in part to the higher margins than its competitors because these fees are also counted in the “Fee-Related Revenue”.

Comparing Distributable Earnings (DE) Multiples

Although the FRE margins of KKR are industry frontrunners, and its revenues and net income are also increasing in double digits, it is still trading at a discount relative to other companies.

The reason it is being priced at a premium over Apollo (NYSE:APO) is due to the FRE mix. In other words, Fee-Related Earnings constitute 75% of the earnings of KKR whereas they are just 45% of Apollo’s earnings since the latter is more dependent on Spread-Related Earnings ((SRE)). And this makes a lot of difference when valuing asset managers, and justifiably so.

Fee-Related Earnings are deemed superior because they are less volatile and stickier than SRE. Simply put, the greater the concentration of FRE in total earnings, the greater the premium paid.

If you look at BAM, it is priced the most expensive among its peers (around 33x). And the reason is that nearly all of its revenues are fee-based. Blackstone comes second, with FRE concentration of around 85%.

Historical Valuation vs Present

Just to be clear, the triple-digit DE growth of KKR in 2021 was because of

its take-over of Global Atlantic that added approximately $90 billion to its asset base

Private Equity firm exits were at the optimal level which contributed significantly to KKR.

the Capital Markets business produced lucrative revenues since IPOs were at their peak.

During the next two years, however, the exits and M&A activity decelerated considerably because interest were at their peak and consequently, the cost of capital went up.

This had a negative impact not only on KKR but on all other asset managers as well. In 2024, the growth rates began to improve as the interest rates began to fall.

To determine the present valuation of KKR, I have considered the TTM Distributable Earnings of $5.45 to be the starting point.

Since the stock is currently trading near $114, there is a discount of approximately 14% from the midpoint of $133.21. Even if Distributable Earnings grow at 12% for the next five years, we’re looking at a 15% annual return at today’s prices.

What’s Next?

To understand where KKR is heading, I looked into its recent press releases, and this undertaking was very helpful indeed.

To begin with, I believe the company will be much more active in the Middle East especially Saudi Arabia and the GCC (Gulf Cooperation Council). This can be seen by the recent news of the company having a major financing agreement of $550 million with ACWA Power. Not only that, it also expanded its presence in the region with a new office in Abu Dhabi.

Secondly, it has been pouring a lot of money into energy, data centres and warehouses, which are all in high demand at present. Plus these asset classes are projected to be expanding in the coming years quite a lot.

Moreover, KKR is becoming an active seller of its investments in businesses such as OneStream that IPO’d in 2024 and MasOrange. I believe that these exits will greatly increase the Distributable Earnings and therefore bring cash to the company that it can invest in the future.

Risks

No doubt, I strongly believe that KKR has immense potential to provide excellent returns in future, but there are also certain risks that are good to know in advance. The majority of the risks that I see for KKR are macroeconomic business risks, which are common to all asset managers in general, interest rates being the most prominent among them. High interest rates may create enormous turbulence in the business of KKR, as it did in 2022 and 2023.

If you look at KKR’s beta, it is 2.0. In simple terms, it is two times more volatile than the S&P 500 index. Unless you are an investor who does not mind sharp upswings and downswings, KKR might not be the right investment for you.

Another KKR-specific risk that I see is the underperformance of its funds. In a situation where a fund managed by KKR doesn’t perform well, it has to pay back investors, what is usually called a clawback.

However, despite these risks, I think KKR’s experience and strong position in the industry will help it immensely to do well in the long term.

The Bottom Line

I genuinely believe that KKR is one of the best asset managers in the market. The southward movement of KKR’s stock stems from worries about private credit industry and weak sentiment towards alternative managers, not due to fundamental issues in KKR’s business.

It has great margins, revenues and net income are increasing in the double digits and it is trading below its intrinsic value.

If you are an dividend investor, the ~0.6% dividend yield of KKR might not be attractive enough. However, If you are targeting capital appreciation, I strongly think KKR can achieve returns that outshine the market in the next five to ten years.