One Dividend Stock I’m Buying Aggressively

With a 4.26% dividend yield combined with the recent 15% dividend hike and 15%+ targeted stock price appreciation, this stock is a must buy at current prices.

Due to the persisting negative sentiment towards private credit, stocks of some really high-quality asset managers have come down significantly. And this decline has created a strong buying opportunity for investors who are willing to look beyond weeks and months.

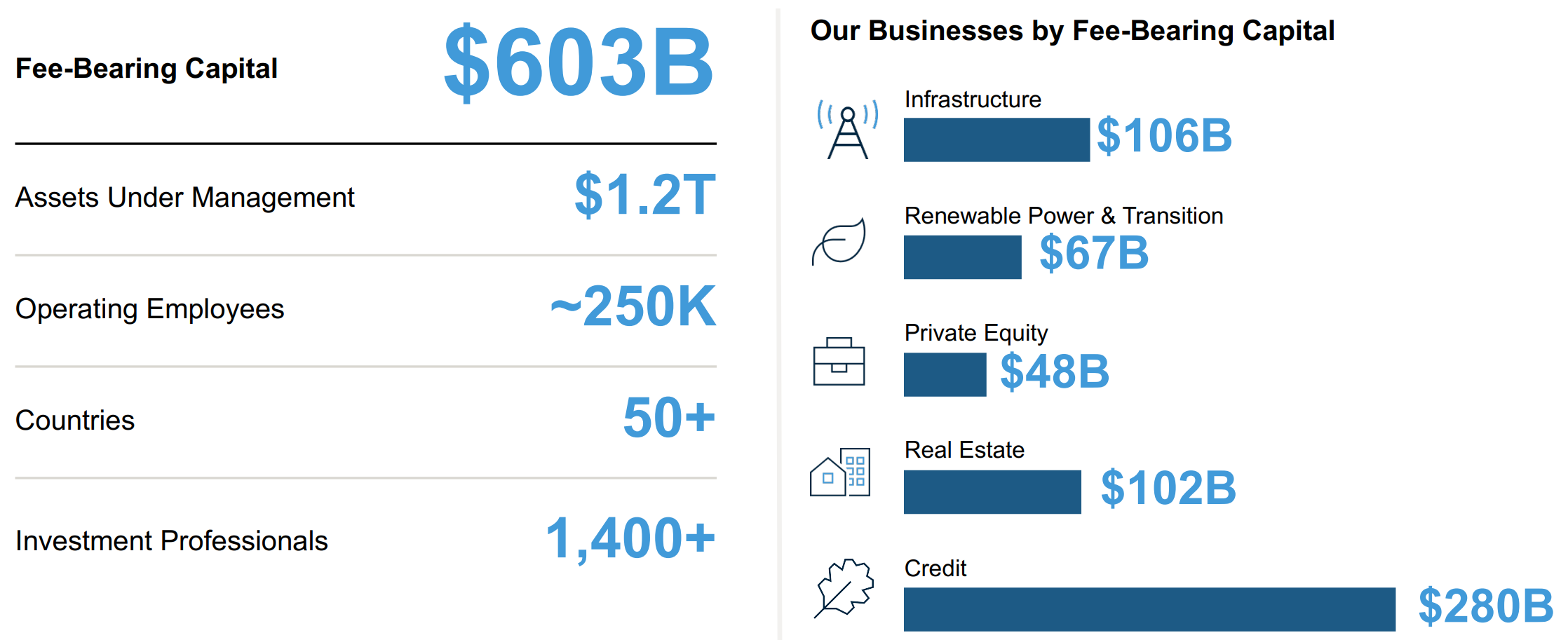

One such stock is Brookfield Asset Management (NYSE: BAM, TSX: BAM). If you haven’t heard about it before, I’ll introduce it briefly. So, BAM is an alternative asset manager, meaning it raises funds from institutions like pension funds, sovereign wealth funds, and high-net-worth individuals to invest in private credit and equity, and real assets like real estate, energy, and infrastructure.

The way BAM generates revenue is by charging base management fees on the funds that it manages and performance fees through carried interest, once a preset hurdle rate of return is crossed.

Now, even though the stock has fallen significantly over the past year, the underlying business is actually thriving, and this is the kind of opportunity that long-term investors wait for; fundamentals up, price down.

The Fundamentals

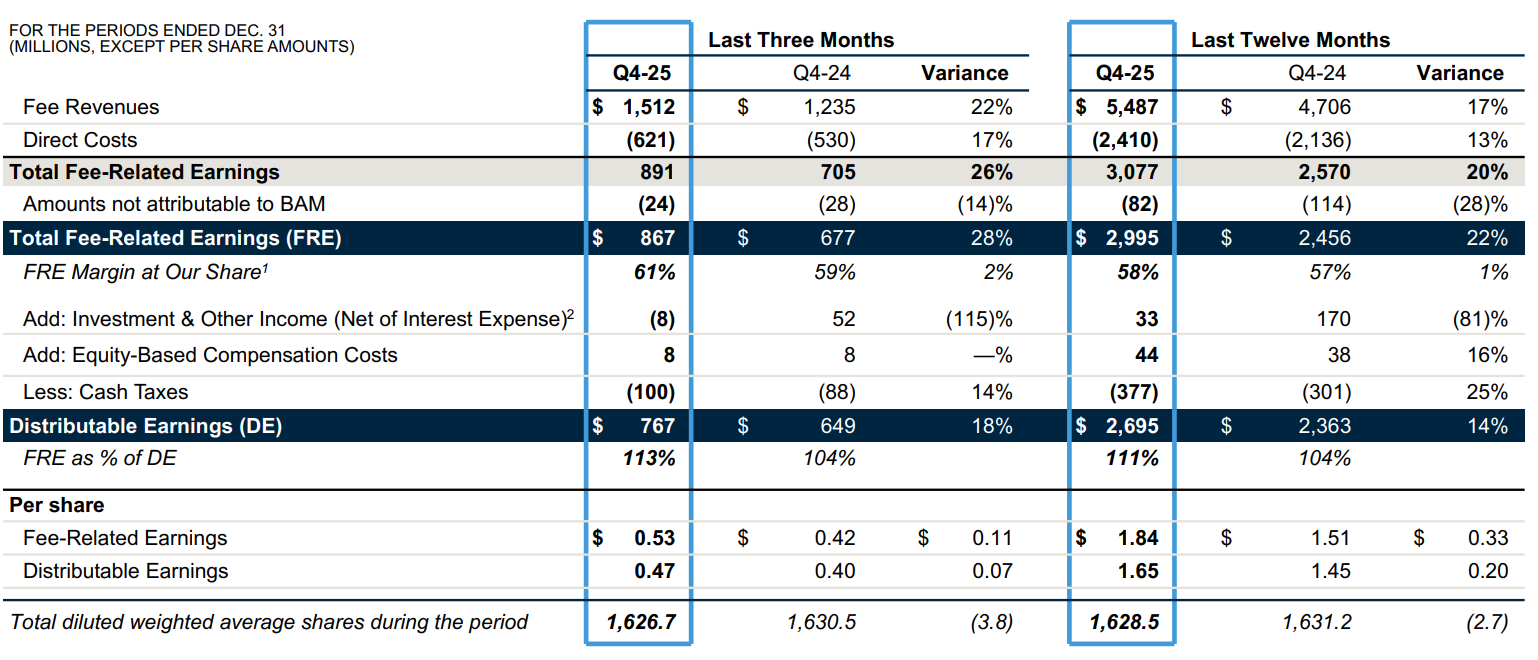

For the full year 2025, Fee-Related Earnings were up 28%, and Distributable Earnings were up 14%.

Despite the ‘scary headlines’ about private credit and equity, BAM had a strong fundraising year and raised $112 billion in 2025. Not only that, Dry powder, which is the capital that BAM can deploy, is now $134 billion.

In short, the fundamentals are consistently improving, whereas the stock price is failing to catch up due to overall negative sentiment towards the industry.

The Dividend

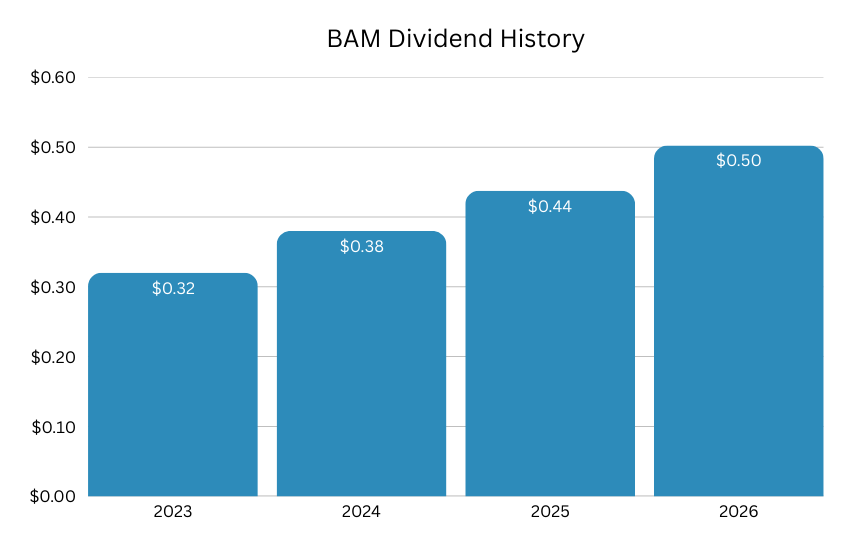

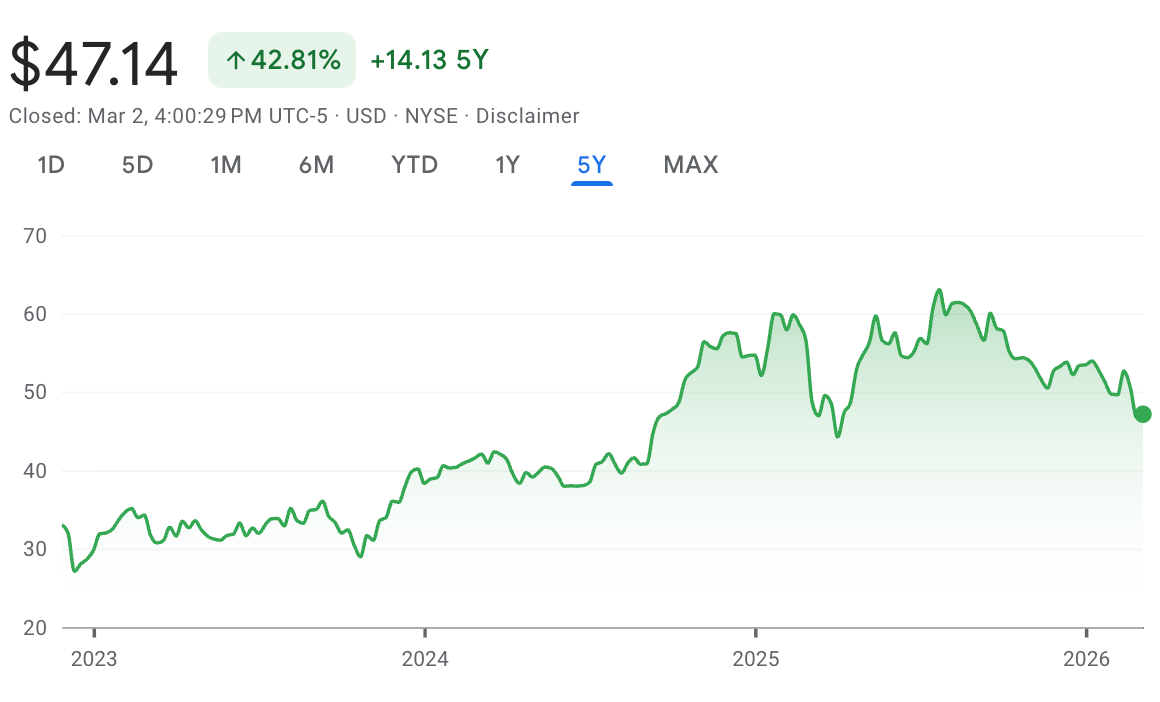

After the most recent 15% hike, BAM now pays a quarterly dividend of $0.5025 / share or an annualized distribution of $2.01. At its current share price of $47.14, the dividend yield is 4.26%, which makes BAM an excellent addition to a passive income portfolio.

What makes the dividend even more attractive is the fact that it has been growing consistently since 2023. It has gone up from 32 cents to about 50 cents each quarter, representing a total increase of 56% in just three years and a CAGR of 16%. Plus, the management has been quite clear about its intention to keep increasing the dividend as the business continues to grow.

Payout Ratio

Brookfield’s management plans to distribute 90-95% of the distributable earnings of BAM as dividends to shareholders. Now, in most cases, I find such a high payout ratio to be quite unsettling because it could create a hindrance in future growth opportunities. However, since BAM is an asset-light business that doesn’t need much of its own capital to grow, I’m not concerned about the high payout ratio.

Since the payout ratio is a percentage of distributable earnings and the management expects to compound them annually at 15%, I’m quite confident about dividends growing at a similar pace.

Capital Appreciation

Now, just to make it clear, my goal isn’t to recommend you stocks with the highest yield, but stocks where I expect a stable, growing dividend, a safe payout ratio, plus the potential for capital appreciation. In BAM, I see all of these qualities. Yes, the stock has performed poorly over the past year, but if we zoom out a little bit, the stock is still up about 43% despite the recent slump. I’m pretty confident that once the private credit worries pull back and sentiment turns positive, BAM has significant upside.

Conclusion

Long story short, I strongly believe that BAM is an excellent business which continues to grow consistently. The stock price decline isn’t because of fundamental weakness within the company but due to the negative sentiment toward private markets, which is affecting all alternative asset managers today.

In my opinion, this sentiment-driven price movement is a solid buying opportunity where you get to lock in a 4.26% dividend yield plus the potential to compound capital at superior returns.